Multi Trip vs Single Trip Travel Insurance: Which One Actually Makes Sense?

Disclaimer: I worked in the insurance industry for 15 years, so I tend to read policy details a little more closely than most people. But I am not an insurance agent or attorney, and this article is for informational purposes only. Coverage, definitions, and pricing vary by policy and state, so always review the full policy details before purchasing.

Multi-trip vs single trip travel insurance sounds like a small decision. One covers a single vacation. One covers multiple trips in a year.

The real difference shows up when you look at how often you travel, how long your trips last, and how much prepaid money you’re trying to protect.

That’s what we’re going to break down here.

If you’re still figuring out whether you need travel insurance at all, start with the Travel Insurance Guide first.

What Is Single Trip Travel Insurance?

Single trip travel insurance covers one specific trip.

You enter your travel dates, total prepaid trip cost, ages, and destination. The policy is built around that one set of travel details.

If you take another trip later in the year, you buy another policy.

I’ve shared my full travel insurance claim experience if you want to see how a real claim actually plays out.

How It Works

You choose:

- Departure and return dates

- Total prepaid trip cost

- Travelers and their ages

The premium is based on those details.

It is designed specifically for that trip.

What It Typically Covers

Most comprehensive single-trip policies include:

- Trip cancellation

- Trip interruption

- Emergency medical

- Emergency evacuation

- Baggage loss/delay

Trip cancellation coverage usually matches the total insured cost of your trip.

If your trip costs $5,000, your cancellation limit is typically $5,000. If it costs $12,000, it scales accordingly.

That structure becomes important when you compare it to multi-trip coverage.

If you’re relying on a credit card for some of these protections, here’s how credit card travel insurance actually works.

What Is Multi Trip Travel Insurance?

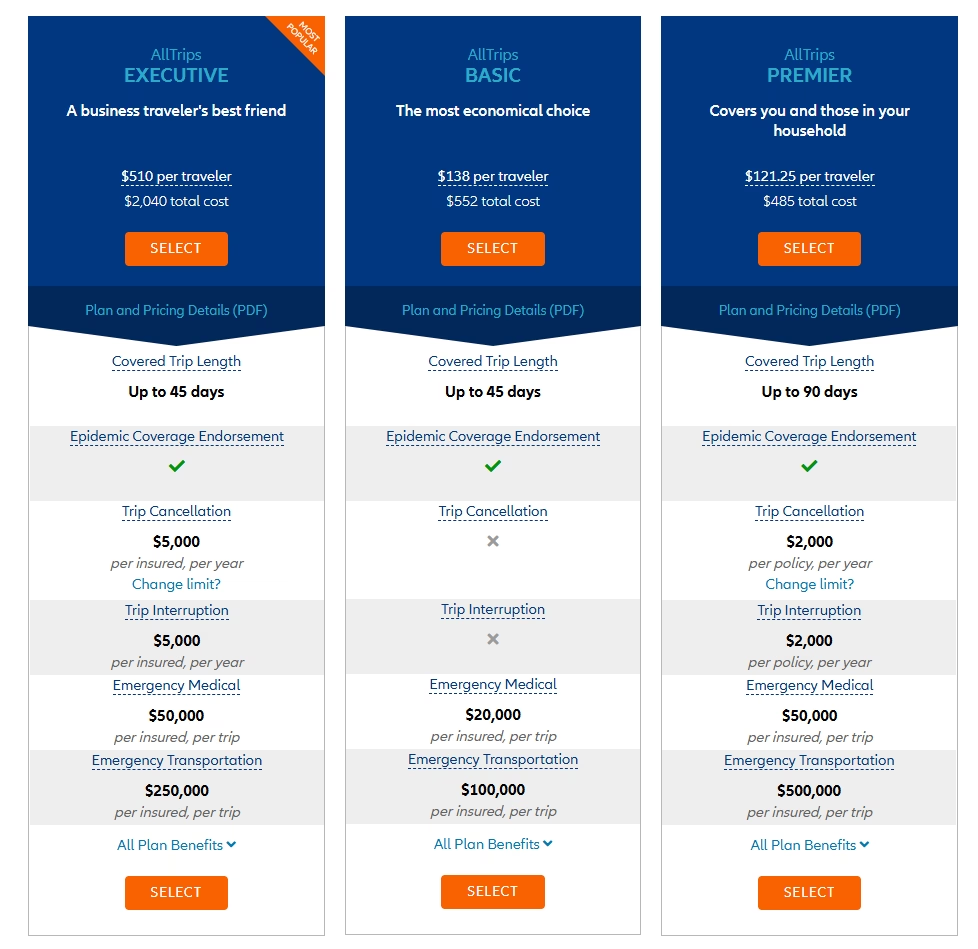

Multi trip travel insurance, often called annual travel insurance, covers multiple trips taken within a 12-month period.

You pay once. Coverage lasts for a year.

How It Works

A multi-trip policy:

- Covers trips within a 12-month window

- Sets a maximum trip length per trip, often 30 to 75 days

- Prices primarily based on age and selected coverage limits

If you travel again during the year, you do not need to purchase another policy as long as each trip stays within the allowed trip length.

Important Coverage Differences

This is where multi trip vs single trip travel insurance becomes more nuanced.

There are generally two types of multi-trip policies.

Medical-Focused Annual Plans

These are built mainly to cover:

- Emergency medical treatment

- Hospital visits

- Emergency evacuation

They often include little or no trip cancellation, trip interruption, or baggage delay or loss coverages.

These plans are designed to protect you medically while traveling, not to reimburse a large prepaid vacation.

That is one reason multi-trip insurance can appear cheaper.

Broader Annual Plans

Some multi-trip policies include:

- Trip cancellation

- Trip interruption

- Baggage benefits

However, they usually do not automatically match each trip’s full prepaid cost.

Instead, they may:

- Cap cancellation per person

- Cap cancellation per trip

- Set a maximum amount for the year

So if you take a $12,000 trip, the policy may not insure the full $12,000 the way a single-trip policy would.

The structure is different.

| Feature | Single Trip | Multi Trip |

|---|---|---|

| Coverage Duration | One specific trip | Multiple trips over 12 months |

| Trip Length Limits | Based on your exact travel dates | Per-trip cap, often 30 to 75 days |

| Trip Cancellation | Matches your insured trip cost | May be capped per person, per trip, or excluded |

| Medical Coverage | Commonly $100,000 to $500,000 or more | Varies widely, some plans are medical-only |

| Evacuation | Often $250,000 to $1,000,000 | Varies by plan |

| Cost Structure | Pay for each trip | One annual payment |

| Convenience | Buy coverage as needed | Buy once for the year |

| Best For | Infrequent or expensive trips | Frequent shorter trips |

Cost Comparison: When Does Multi Trip Insurance Save Money?

These examples reflect realistic sample quotes for U.S.-based travelers. Coverage limits and pricing vary by age, state, and plan, but this is meant to give you an idea so you can price your own detail-specific quotes with more context.

Before we look at pricing, a quick note.

Annual policies are structured differently depending on the plan. For these examples, I used the strongest comparable annual option available in each scenario.

In some cases, that means comparing comprehensive single-trip coverage to an annual plan that emphasizes medical benefits more heavily than cancellation. That’s simply how many annual policies are structured.

The goal isn’t identical coverage. It’s to show how pricing shifts based on travel frequency and needs.

Here’s what the numbers showed.

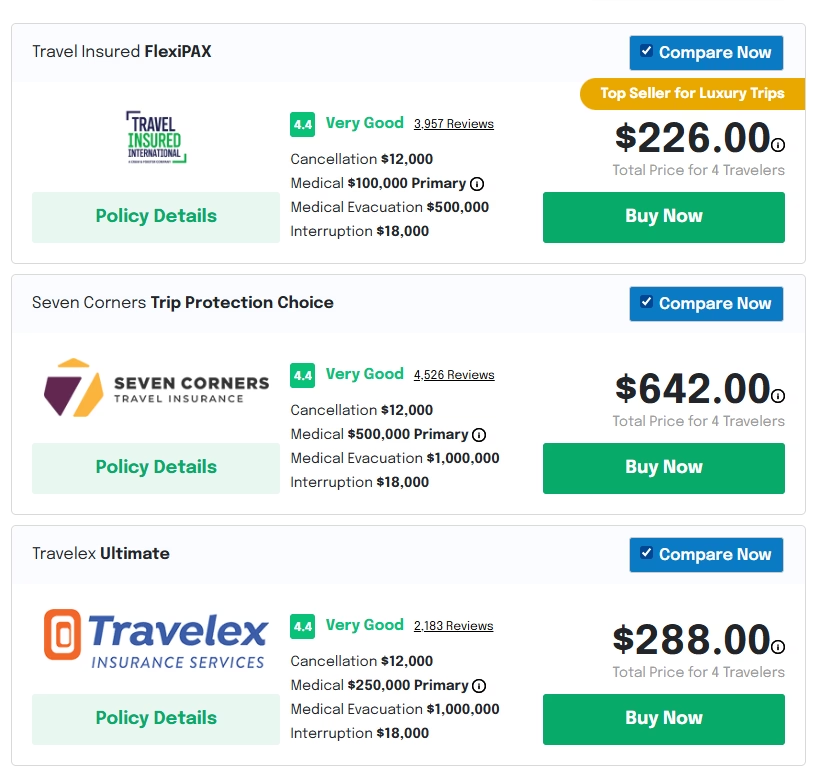

Scenario 1: One Large International Family Trip

Family of four

Ages 40, 40, 10, 5

12-day trip

$12,000 total cost

Comprehensive single-trip policies ranged roughly from $250 to $700, with many solid mid-level plans between $325 and $550.

Comparable annual options for the same family were approximately $450 to $600 for the year. Those annual policies often structure cancellation differently than single-trip coverage, which is why looking at the coverage details matters just as much as the price.

With a single-trip policy, you are fully insuring that specific $12,000 trip for cancellation, interruption, medical, baggage, and delay.

With an annual plan, cancellation may be capped per person or per trip, and medical limits may differ depending on the structure of the plan.

If you’re only taking one large international vacation, single-trip coverage often fits more cleanly because it aligns directly with that trip cost.

To see how pricing actually compares, I ran sample quotes for a family of four (ages 40, 40, 10, and 5) taking a $12,000 international trip. Here’s a real example of how several policies compare for that trip:

Scenario 2: Three Moderate Trips Per Year

Same family

Three trips

$5,000 per trip

Single-trip policies ranged roughly from $140 to $380 per trip depending on limits.

Three separate policies could total approximately $450 to $1,100 for the year.

To see comparable annual policies, I ran a sample multi-trip quote for the same family.

This is where the math starts to overlap.

If you buy three single-trip policies, each $5,000 trip is fully insured for cancellation based on that trip’s cost.

With an annual policy, cancellation may be structured differently. For example, a plan might cap cancellation at $1,000 or $1,500 per person per trip, even if your actual trip cost is $5,000.

If your prepaid costs are modest, partially refundable, or booked with flexible points, annual coverage can begin to make financial sense.

If you want each trip individually insured at full cost, single-trip policies still offer more precise protection.

Scenario 3: Frequent Travel, Age 68

Couple age 68

Four trips per year

$5,000 per trip

Single-trip policies ranged roughly from $275 to $600 per trip.

Four policies could total $1,100 to $2,400 annually.

Comparable annual options were around $530 for the year.

This is where frequency really shifts the math.

For travelers in higher age brackets, buying single-trip coverage repeatedly can add up quickly.

If your goal is strong medical protection across multiple trips, annual coverage can be significantly less expensive over the course of a year.

If full cancellation matching each trip cost is the priority, you’ll likely pay more overall using single-trip policies.

The Most Overlooked Differences

Trip Length Caps

Multi trip policies limit how long each individual trip can be.

Many cap trips at 30 days. Some allow 45, 60, or 75 days.

If you take a trip longer than the cap, coverage may not extend for the entire duration.

Single-trip policies are tied directly to your exact travel dates, so there is no separate per-trip limit to monitor.

If you ever take longer vacations, this matters more than most people realize.

Cancellation Structure

Single-trip policies typically match cancellation coverage to your exact insured trip cost.

Multi trip policies may:

• Cap cancellation per person

• Cap cancellation per trip

• Cap cancellation per year

• Limit cancellation coverage compared to a single-trip plan

This is one of the biggest structural differences between multi trip vs single trip travel insurance.

When annual coverage looks cheaper, it’s often because the cancellation structure is built differently, not because the policy is automatically better or worse.

Pre-Existing Conditions and Timing Windows

This part is not obvious, and it took me many years to even notice.

Many single-trip policies include a pre-existing condition waiver if you purchase coverage within a short window after your first trip payment, often 10 to 21 days.

If you book your trip in pieces like I always do, flights first and hotels later, that first payment typically starts the waiver clock.

If you miss that window, your options narrow quickly.

A few policies base eligibility on your last trip payment instead, but they are less common and you’re working with whatever other policy limits that specific plan sets.

Annual policies vary. Some include coverage for stable pre-existing conditions. Others exclude them. The wording is different from plan to plan.

There isn’t a shortcut here. You have to read that section carefully.

What If a Travel Companion Has a Pre-Existing Condition?

Let’s say you and the people insured under your policy have no pre-existing conditions. But you’re traveling with another family member or friend who does. They may even have their own insurance.

If that person gets sick during the trip and you decide to go home early or miss part of the trip because of it, your policy may treat that person as a covered “travel companion.” That means their illness could be a valid reason for your trip interruption claim.

But there’s a second layer.

The insurance company will still look at whether that medical issue is considered pre-existing under the policy’s rules.

If a pre-existing condition waiver applies and the timing requirements were met, your interruption claim may be covered.

If the waiver does not apply, the claim connected to that condition may not be paid, even though you personally have no medical conditions.

Also make sure the policy’s definition of “travel companion” includes that person. Coverage depends on that wording.

Cancel For Any Reason Coverage

Cancel For Any Reason, often shortened to CFAR, is usually an optional upgrade on single-trip policies.

It typically must be added shortly after your first trip payment and increases the premium.

Most annual policies do not offer CFAR in the same way.

The sample pricing in the scenarios above did not include CFAR upgrades.

What If Your Credit Card Already Offers Travel Protection?

Before purchasing travel insurance, it’s worth checking what your credit card includes.

Many premium cards provide:

• Trip cancellation

• Trip interruption

• Trip delay

• Baggage delay

I’ve broken this down in detail in my full guide to Chase credit card travel insurance and my Amex credit card travel insurance guide posts.

Most do not provide meaningful coverage for routine overseas medical bills like doctor visits, hospital stays, or prescriptions. Some include evacuation coordination, which is helpful, but that is not the same as covering medical treatment.

If your card already provides cancellation protection and you’re comfortable with its limits and requirements, you might choose to purchase standalone travel medical coverage instead of a full comprehensive plan.

Rental Cars: Collision vs Liability

Rental car coverage is another area people assume is handled automatically.

There are two separate protections to think about.

Collision Damage Coverage

This covers damage to the rental car itself.

Many premium credit cards include collision damage coverage if you pay for the rental with that card and decline the rental company’s damage waiver.

That can allow you to skip the rental counter’s expensive collision add-on. This coverage can also be added to some single-trip travel insurance policies, usually for an additional cost.

Liability Coverage

Liability covers damage or injuries you cause to other people.

Most travel insurance policies do not cover rental car liability. Most credit cards do not cover rental car liability either.

Imagine driving on a narrow road and accidentally sideswiping another vehicle. Their car is damaged and someone is injured.

Without liability coverage, you could be responsible for repairs, medical bills, and legal costs.

If you are renting in the United States, your personal U.S. auto policy may extend liability coverage to rental cars. It’s worth confirming before you travel.

If you are renting internationally, your personal auto policy often does not extend outside the country.

Some countries (like the United Kingdom) require rental companies to include liability coverage in the base rate by law. Others do not.

It’s easy to assume something covers this. It’s better to confirm before you get behind the wheel.

When Multi Trip Insurance Makes Sense

Multi trip coverage often makes sense if:

• You travel three or more times per year

• Your trips are shorter than the plan’s per-trip limit

• Your primary concern is medical coverage

• Your prepaid costs are relatively modest

• You already have cancellation protection elsewhere

When Single Trip Insurance Is Smarter

Single-trip coverage often makes more sense if:

• You take one or two trips per year

• You have a large prepaid vacation

• You want cancellation to match your exact trip cost

• You want CFAR (cancel for any reason) as an option

• You prefer coverage tied directly to specific dates

Packing It Up

When deciding between annual multi trip vs single trip travel insurance, focus on four things:

• How often you realistically travel each year

• How long each trip lasts

• How much prepaid money is at risk

• Whether your main concern is cancellation, medical coverage, or both

There isn’t a universal right answer.

There’s just the version that fits how you actually travel.

Your Next Read

Real Travel Insurance Claim Experience: How We Recovered $2,615 After a Spain Trip Disaster

How Does Credit Card Travel Insurance Work? Everything You Need to Know

Chase Credit Card Travel Insurance: Coverage Limits and Differences by Card