Amex Travel Insurance Explained (2025): Card List & Coverage Guide

Amex travel insurance enjoys a reputation for being among the most comprehensive credit‑card travel protections on the market—but how does it perform in the real world? Which American Express® cards with travel insurance actually deliver, and is the coverage as seamless as the marketing suggests?

As a former Underwriter who’s analyzed too many insurance policies and contracts, I’m here to decode the fine print for you. In this guide, I’ll translate the legalese into English, highlight the essential Amex travel insurance benefits, compare Amex travel insurance vs Allianz (and other standalone policies), and flag the details you can’t afford to miss—so you can decide if the built‑in perks are all you need or if a separate policy still deserves a spot in your carry‑on.

This post mentions credit‑card products from American Express®, Chase®, Hilton®, Marriott®, Delta®, and other financial institutions. All trademarks belong to their respective owners, and Journey Currencies is not endorsed by or affiliated with these brands unless stated. Opinions are our own; content is educational, not financial advice. Always review your card’s Guide to Benefits for current terms.

What Is Amex Travel Insurance?

Amex travel insurance benefits come automatically on a handful of American Express travel cards—no extra fee or forms required. Think of them as a built-in safety net covering trip delays, trip interruption or cancellation, baggage hiccups, and car-rental damage. When your flight sits on the tarmac for hours or your backpack decides to tour Paris without you, American Express trip insurance can help foot the bill for meals, hotels, or replacement essentials.

How Does Amex Travel Insurance Work?

- Pay for your round‑trip travel with an eligible Amex card.

- Save receipts and documentation (delay notices, baggage reports, etc.).

- Claim online or by phone if a covered mishap occurs.

Remember, Amex protections are secondary—they jump in only after refunds or other insurance have paid.

Pro tip: snap photos of receipts as you go; you’ll likely have to digitize them for a claim anyway (or just put them all in a ziplock like I did when I knew I’d be making a claim)

Comparing Amex Travel Insurance to Stand‑Alone Policies

Not every American Express card provides the same protections, but here’s what you’ll generally find when you stack typical Amex benefits against a stand‑alone policy.

| Coverage Type | Typical Amex Card | Stand‑Alone Policy (e.g., Allianz) |

| Trip Delay / Cancellation | Included on Platinum‑family & many premium co‑branded cards.Limits range $300–$10,000 depending on the product. | Included; you choose the trip‑cost limit when buying the plan. |

| Lost / Delayed Baggage | Included on most Amex travel cards.Standard limits $500–$1,250; premium cards up to $3,000. | Included (commonly $1,500–$2,500). |

| Rental‑Car Damage (CDW) | Included but almost always secondary.You must decline the agency’s CDW/LDW. | Optional add‑on or bundled in higher‑tier plans; usually primary. |

| Emergency Medical Care | Not provided on any U.S.‑issued Amex card. | Included—often $50k–$1 M in medical expenses. |

| Medical Evacuation | Up to $100k on select premium cards (Platinum‑family, Centurion®, Hilton Aspire, Marriott Brilliant®, Delta Reserve). Most other Amex cards offer none. | Included—typically $250k–$1 M. |

Cost Snapshot: Free Perk vs Paid Policy

- Amex travel insurance: $0 extra once you hold an eligible card. The coverage is included for free, no enrollment or premium, although the card’s annual fee (anywhere from $0 to $695) still applies.

- Stand‑alone policy (e.g., Allianz): Typically 4 – 10 % of your total trip cost, influenced by age, destination, and length. Example: a OneTrip Prime plan for a $3,000, two‑week international vacation for a 35‑year‑old traveler runs roughly $140–$180.

Why it matters: If you already pay an Amex annual fee, the built-in coverage is a no‑brainer if it makes sense to pay for the round trip with that card. But if you need medical protection—or a higher evacuation cap—the paid policy can still be a smarter value.

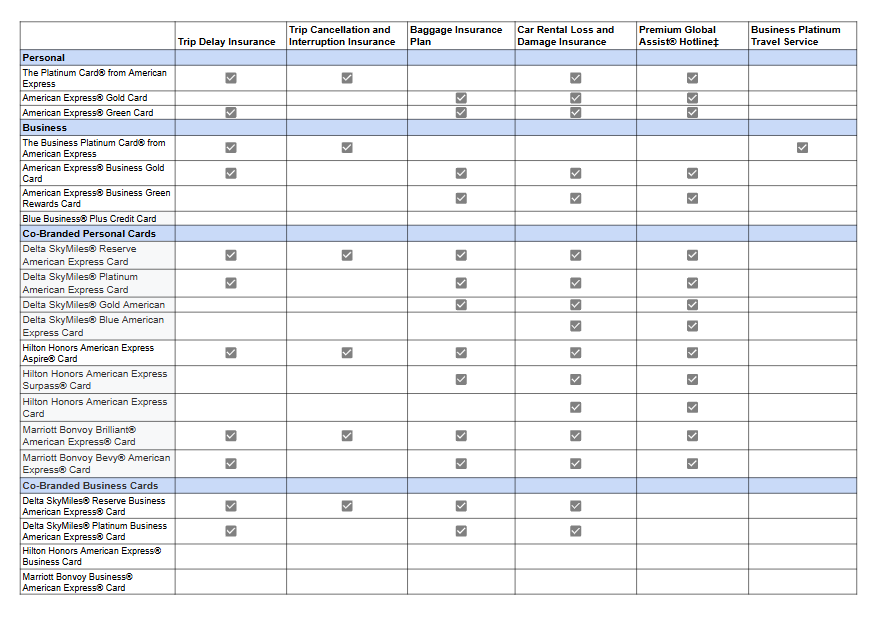

Which American Express Credit Cards Offer Travel Insurance?

Personal & Business Core Cards

- The Platinum Card® from American Express

- American Express® Gold Card

- American Express® Green Card

- The Business Platinum Card® from American Express

- American Express® Business Gold Card

- American Express® Business Green Rewards Card

- Blue Business® Plus Credit Card from American Express

Co‑Branded Personal Cards

- Delta SkyMiles® Reserve American Express Card

- Delta SkyMiles® Platinum American Express Card

- Delta SkyMiles® Gold American Express Card

- Delta SkyMiles® Blue American Express Card

- Hilton Honors American Express Aspire® Card

- Hilton Honors American Express Surpass® Card

- Hilton Honors American Express Card

- Marriott Bonvoy Brilliant® American Express® Card

- Marriott Bonvoy Bevy® American Express® Card

Co‑Branded Business Cards

- Delta SkyMiles® Reserve Business American Express® Card

- Delta SkyMiles® Platinum Business American Express® Card

- Hilton Honors American Express® Business Card

- Marriott Bonvoy Business® American Express® Card

Breakdown of Amex Travel Insurance Coverage

Trip Delay Insurance

(Amex Credit Card Travel Delay Coverage)

If your trip is delayed for a covered reason for a specified time, you may be reimbursed for eligible expenses. Note that even with a valid claim, there are benefit limits.

American Express typically offers two tiers of trip delay insurance:

- 6-hour delay: Up to $500 per trip in eligible expenses

- 12-hour delay: Up to $300 per trip in eligible expenses

Important Amex travel delay insurance rules:

- The trip must be round-trip, beginning and ending in the same city

- The entire trip must be paid with your eligible American Express card

- Only 2 claims allowed per 12-month rolling period

- Coverage is secondary (other reimbursements must be used first)

- Issued by New Hampshire Insurance Company, an AIG company

Common eligible reasons (not guaranteed):

- Inclement weather preventing safe travel

- Equipment failure by a Common Carrier

- Lost or stolen passport

Common non-covered reasons:

- Issues known before your trip began

- Losses due to intentional acts by the traveler

Trip Cancellation and Interruption Insurance

(Amex Trip Coverage)

If your trip is canceled or interrupted due to a covered reason, you may receive reimbursement for nonrefundable expenses.

Amex travel insurance limits:

- $10,000 per trip

- $20,000 per card annually

- Limits apply separately to cancellation and interruption

Key things to know:

- Trip must be round-trip (meaning starting and ending in the same city) and fully paid with your AmEx card

- Secondary coverage only – refunds or vouchers must be used first

- Issued by New Hampshire Insurance Company, an AIG company

Common covered reasons (examples, not guaranteed):

- Military orders or jury duty

- Inclement weather

- Subpoena by the courts

Common exclusions:

- Pre-existing conditions

- Mental health conditions (unless hospitalized)

- Traveling intoxicated or while committing a felony

Baggage Insurance Plan

(Amex Lost/Damaged Luggage Coverage)

This insurance covers baggage that is lost, damaged, or stolen during travel.

Standard Amex card limits:

- Up to $1,250 for carry-on baggage

- Up to $500 for checked baggage

Premium Amex cards (e.g. Hilton Aspire, Marriott Brilliant):

- Limits up to $3,000

Requirements for Amex baggage insurance:

- Full fare for plane, train, bus, or ship must be paid with your Amex card that offers this benefit

- Combining Amex points (Membership Rewards or Pay With Points) is allowed

- Non-Amex points are not eligible (e.g., United miles + AmEx partial payment won’t count)

- Coverage is secondary to airline or carrier reimbursement

Car Rental Loss and Damage Insurance

(Amex Rental Car Protection)

This coverage protects against damage or theft of a rental car in eligible locations.

Key exclusions:

- No coverage in Australia, Italy, or New Zealand

- Does not include liability (at-fault) coverage

To be eligible for Amex travel rental car coverage:

- Entire rental must be paid with the eligible Amex card

- You must decline the rental agency’s optional insurances:

- Collision Damage Waiver (CDW)

- Personal Accident Insurance

- Personal Property Coverage

- Any similar coverage

- Collision Damage Waiver (CDW)

- Renter must sign the agreement and be the main driver

- Coverage is secondary, applies only after other insurance

U.S. Residents: Check with your personal auto insurance—some policies may already cover you when renting a car, especially within the U.S.

Amex Travel Insurance Does Not Include Medical & Dental Care

Need a doctor abroad? Built‑in Amex coverage won’t foot that bill. For evacuation help, see Premium Global Assist® Hotline below.

Premium Global Assist Hotline

Available 24/7, the Amex Travel hotline service provides emergency coordination for medical, legal, and financial assistance while traveling.

24/7 Premium Global Assist Hotline/Customer Service: Toll Free: 1-800-345-AMEX (2639) Direct Dial Collect (Outside US and Canada): 1-715-343-7979

Highlights of Premium Global Assist:

- Must be more than 100 miles from home

- May assist with emergency medical transport (with approval)

- Third-party costs may apply

Emergency Medical Transportation Assistance — What to Expect

American Express tucks this perk inside the Premium Global Assist Hotline section of its card benefits. It’s essentially “on-call” air ambulance service — priceless peace of mind if the unexpected happens. The catch? Only a handful of premium AmEx cards carry it, and the service has a checklist you’ll need to clear first.

Cards That Include the Benefit (2025)

- The Platinum Card® (Personal)

- Business Platinum Card®

- Platinum Card® for Charles Schwab, Morgan Stanley, and Goldman Sachs

- Centurion® Card (Personal & Business)

- Delta SkyMiles® Reserve

- Hilton Honors American Express Aspire

- Marriott Bonvoy Brilliant®

How It Works in Real Life

- You’re 100 + miles from home and experience a serious illness or injury.

- Call the Premium Global Assist Hotline. Their medical team decides whether local care is adequate or an evacuation is necessary.

- If approved, AmEx arranges and pays for transportation — typically to the nearest facility equipped to treat you or, once stable, back home.

Eligibility Checkpoints

To keep expectations realistic, be sure at minimum you can say “yes” to all of these:

- Round Trip paid with the eligible AmEx card (meaning trip starts and ends in the same city)

- Local doctor confirms you’re unfit to continue travel and fit for transport.

- You’re not traveling against medical advice or seeking treatment for a known condition.

- You authorize release of medical records so AmEx’s team can review your case.

What’s Not Covered

- Hospital or doctor bills, prescriptions, or follow-up care.

- Pre-existing conditions or travel undertaken specifically for medical treatment.

Think of it as the flight to safety, not the care while waiting or once you land.

Do a Quick Benefits Check Before You Fly

Coverage details vary slightly by state and card version, so it’s worth five minutes to read the Global Assist® Hotline¹ and Premium Global Assist® Hotline² and Emergency Assistance3 page and find your specific card if you think you may want to rely on this benefit.

That small homework now can save a lot of confusion later — and lets you travel with confidence, not crossed fingers. I doubt anyone wants to search through Terms & Conditions while dealing with an illness or injury that may require emergency transportation.

Business Platinum Travel Service (Bonus Perk)

Exclusive to the Business Platinum Card®, Platinum Travel Consultants can put together complex itineraries, award bookings, and emergency re‑routes—handy when delays trigger insurance claims.

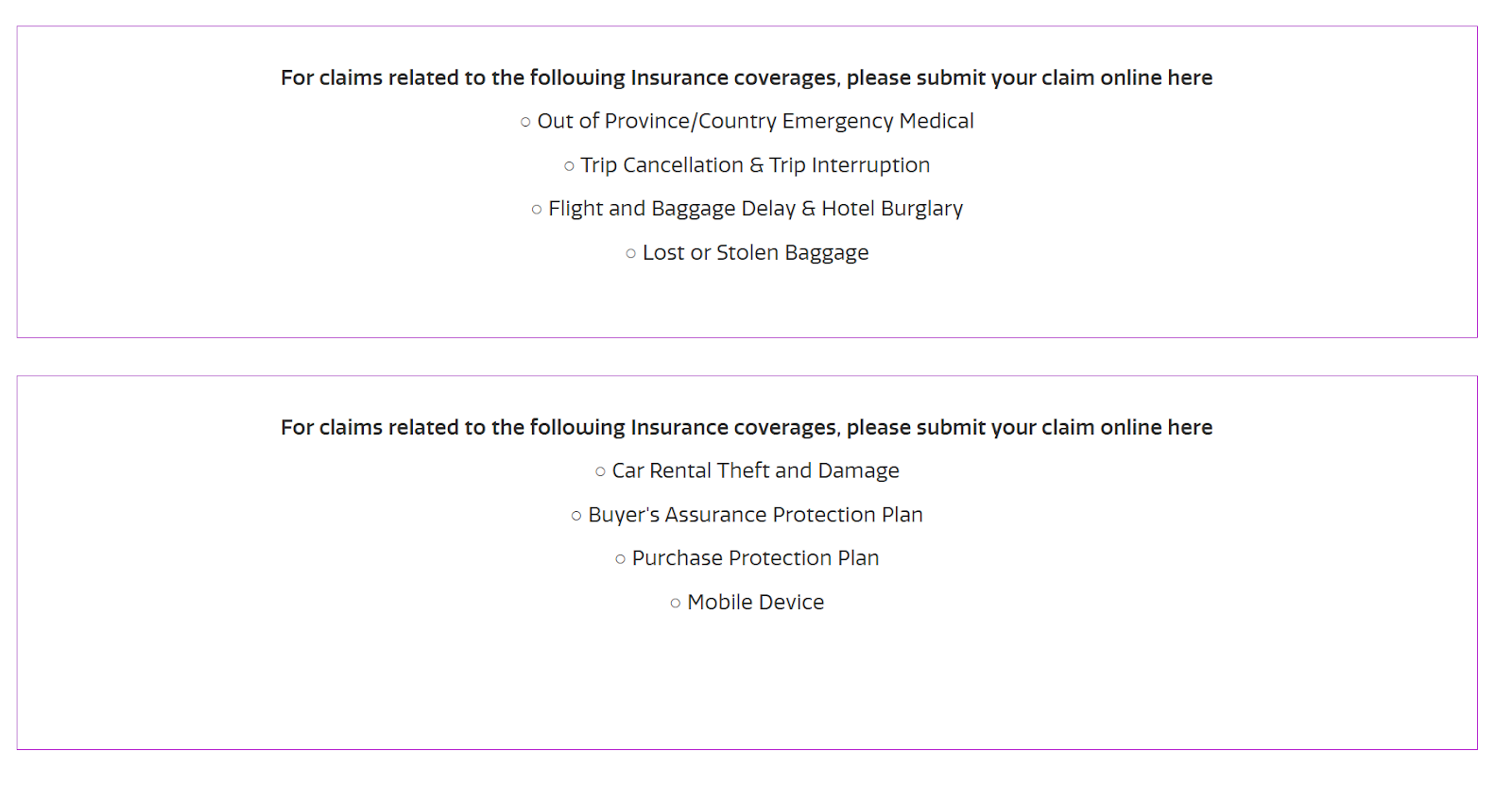

How to File a Claim

- Phone (US & Canada): 1‑800‑243‑0198

- International Collect: (905) 475‑4822

- Online: Link through your Amex account → Benefits & Insurances → Make a Claim Amex Claim Website

You can start a claim, save progress, or check status from the same portal.

Have receipts, delay statements, and proof of other reimbursements ready.

Amex Travel Insurance Exclusions to Know

- Coverage is secondary—if the carrier pays in full, Amex likely won’t.

- Trip must qualify as a round trip (start and end in the same city) and all paid on the card for coverages to be eligible.

- Pre‑existing conditions, traveling while intoxicated, or intentional acts void many benefits.

Is Amex Travel Insurance Enough?

If you rarely leave the U.S., stick to carry‑on bags, and want a buffer for weather delays, Amex might be plenty. I personally layer a stand‑alone policy on every international trip for medical coverage—learned after a medical disaster situation in Spain. Read all about that stand-alone policy claim process here.

Our Travel Insurance Claim Experience: $2,615 Reimbursed

Car renters: I skip Amex’s secondary CDW and swipe a card with primary coverage (hello, Capital One Venture X or Chase Sapphire Preferred/Reserve).

Who Benefits Most from Amex Travel Insurance?

- Travelers who charge all trip costs to a single Amex card

- Frequent domestic flyers who mainly worry about delays

- Carry‑on‑only adventurers

- Organized planners who already have airline or elite‑status protections but want an extra safety net

Points & Miles Travelers: Where Amex Coverage Fits In

If you dream in award charts and track welcome bonuses in color‑coded spreadsheets, you already know the golden rule: every swipe has a purpose. Amex’s built‑in insurance is just another lever in the game—lean on it when it adds value, ditch it when another card scores you more points or better coverage.

If You’re Already Deep in Points & Miles

- Minimum‑spend juggling: When you’re working on a fresh welcome bonus from another issuer, that card should probably get the airfare or hotel charge—meaning Amex protections sit out. Decide purchase‑by‑purchase: chase the points, or lock in the insurance?

- Primary rental‑car coverage: Chase Sapphire Preferred/Reserve and Capital One Venture X beat Amex’s secondary CDW. Swipe one of those solely for the rental car, then decide where the rest of the trip spend belongs.

- Award bookings & refunds: Third‑party insurers won’t redeposit your points or miles, and Amex only reimburses forfeited Membership Rewards®. Luckily, programs like Hilton Honors and United MileagePlus often redeposit awards for free or a modest fee. Keep that in mind when valuing “coverage” on an award ticket.

- Taxes‑and‑fees workaround? Not with Amex. Some cards (think Chase) extend flight coverage if you pay just the taxes and fees with the card. Amex requires that the entire round trip be paid with the card or Amex Membership Rewards points for benefits to trigger.

If You’re New to Points & Miles

- Pick one reward‑heavy Amex (Platinum, Hilton Aspire, etc.) so you earn points and unlock the insurance in one swipe.

- Hit the annual‑fee math: If the card’s perks and insurance save you more than the fee, you’re ahead before earning a single point. Start here: Amex Platinum for Budget Travelers: A Low Spender’s Honest Review

- Layer on a stand‑alone policy for overseas trips until you’re comfortable tracking multiple cards and benefit guides.

Also Check Out: Chase Credit Card Travel Insurance: The Ultimate Guide (2025)

FAQs About Amex Travel Insurance

Does Amex travel insurance cover flight cancellations?

Yes—if your Amex card includes trip cancellation insurance **and** you paid for the round-trip entirely with the card or with Membership Rewards® points. Coverage is typically up to **$10,000 per trip** on eligible cards.

Which Amex cards offer the best travel insurance?

Premium cards like **The Platinum Card® from American Express**, **Hilton Honors American Express Aspire® Card**, and **Marriott Bonvoy Brilliant® American Express® Card** combine strong trip-delay, baggage, car-rental, and evacuation benefits.

Does Amex travel insurance work for international travel?

Yes, but it only covers logistics (trip delay, cancellation, baggage, rental car). It **does not** cover medical or dental treatment abroad—pair it with a stand-alone medical policy if you’re leaving the country.

Is Amex travel insurance primary or secondary?

It’s **secondary**. Amex reimburses you only after the airline, hotel, tour operator, or any other applicable insurance has paid out first.

Can I get coverage if I book my flight with points?

Only if the points are **Amex Membership Rewards®** and the entire round-trip fare (or the entire points redemption) is on your eligible Amex card. For other programs (United MileagePlus, Hilton Honors, Avios, etc.), Amex will not reimburse lost points—rely on the airline or hotel to redeposit them.

Packing It Up

Amex travel insurance can be a solid, cost‑free layer of protection—especially for U.S. trips where medical and auto insurance policies may transfer some benefits as well. Just know its limits. For anything beyond this, a stand-alone policy may be a wise addition.